How SML confused Ghanaian professors

Despite sparring for months with SML, I had never had the privilege of an encounter at close range. Unlike the good souls at the Fourth Estate, whose collaboration with ACEP was backed by IMANI, and who had the opportunity to visit SML a number of times, and in true journalistic fashion, gave all sides a careful hearing.

But once all the evidence has been put together, and troves of documents are ready to be analysed, it becomes the province of us policy analysts to make sense of it all with an eye on public interest and practical outcomes. The policy analysis work is thus inherently interdisciplinary. Anyone who has followed the SML work carefully would have noticed, at least, the following subject matters making frequent appearances:

.General Finance

.Tax Economics

.Supply Chain integrity

.Anti-fraud controls

.Accounting controls

.Petroleum Taxation

.Tax Evasion

.Electronic sensors

.Enterprise Resource Platforms

.Information Technology (IT) integration

.Public Finance

.Corporate Governance

.Public Finance Management

.Procurement Standards

etc etc etc

And, yet, in the end it is a policy matter for which clear executive actions are required. The work of multidisciplinary teams must be effectively synthesized by someone, a policy analyst, with the capacity to quickly ramp up in these areas well enough to be able to piece together the best work done by others and synthesize their content for a non-specialist audience. Media coverage, as well as investigations, would be much poorer without the synthesising power of the policy analysis profession in Ghana.

Yet, in Ghana, this whole thing confuses people. They cannot discern the difference between integrated thinking and Jack-of-all-trades posturing. I wrote a piece about this sometime ago that I feel most people interested in public affairs must read.

The point about integrated thinking is critical in this SML saga, a case where the government of Ghana awarded a billion-dollar contract to an obscure company to fight tax fraud in multiple sectors. A quick recap might be useful for those who haven’t even followed the controversy.

SML was formed in early 2017, conveniently at the dawn of a new government. In barely two months, it had already been tapped by the government, without public tender, to take over a lucrative “revenue assurance” gig awarded by the previous government. When the procurement regulator resisted, SML was smuggled in anyway, as a subcontractor, and then eventually given the job, without regulatory approval.

A need to dramatically expand the contract to give the company a stake in every barrel of oil and ounce of gold and other minerals produced by Ghana compelled the government to push the procurement regulator for approval, and for the first time secure the consent of the board of the state agency that was the ostensible party to the agreement, the Ghana Revenue Authority (GRA). Unfortunately, for all involved in the scheme, ACEP got wind of it and teamed up with the indomitable investigative journalists at the Fourth Estate to investigate. To mixed reactions, the President of the country tasked KPMG, one of the Big Four global professional services firms to investigate the whole affair.

The essential bottomline of the KPMG’s factual findings, which the government refuses to release in the original, and were only summarised in a presidential “whitepaper” is straightforward:

The contract is illegal.

The contract is illegal because the eventual approval by the procurement regulator (PPA) and the Board does not serve to retrospectively cleanse of the earlier legal failings.

The contract is illegal because under Ghanaian law a contract of that nature should have Parliamentary approval.

The contract is substandard because no needs analysis, nor value for money assessments, have ever been performed prior to and following its award.

Had KPMG left things at that, I wouldn’t be writing this essay. But, despite its conflict of interest situation (as a client of one of the parties heavily implicated in this whole affair, the GRA), it apparently proceeded to draw various contentious conclusions about the merit of the arrangement, if only the legal flaws can be cured. Caution note: no one except the President, his handlers, and KPMG have seen the original report.

According to the Ghanaian President’s version of what KPMG said, the consultancy concluded that there is a need for SML’s services in some form because, since SML started working, there has been an incremental growth in the volumes of refined petroleum consumed in Ghana subject to petroleum taxes, and therefore of the amount of taxes paid to the government.

Supporters of the SML cause have latched on to this claim and have mounted a vigorous PR campaign to declare victory for the company. That is understandable. More perplexing is how a train of senior academics at Ghana’s universities joined the bandwagon.

My double encounter with the lead spokesperson of SML has clarified for me how the persuasive magic was performed, and it is linked directly to the discussion above about “integrated thinking”.

To re-emphasise: it is entirely natural, even inevitable, for academic specialists, including top professors, to be functionally incapable of policy analysis after they have spent many, many, years cocooned in their academic specialty. They start to force every complex issue through their own disciplinary lens.

One eminent political scientist has started promoting a theory in which everyone opposed to SML is somehow a geopolitical pawn of international capital. Another professor, a finance PhD, and Dean of one of the two leading public administration schools in Ghana, has embraced the central claim of SML wholeheartedly, producing the below chart to establish how SML’s work has “raised the taxable volumes of petroleum” consumed in Ghana.

The analysis of the Dean (the one with the finance background) is almost entirely identical to SML’s inhouse productions:

The charts above are at the heart of the debate on whether SML deserved to be paid more than ONE BILLION GHANA CEDIS (more than a $100 million at constant prices). The implied questions are whether:

The claim that SML’s work has led to “taxable volumes” of refined petroleum products in Ghana (i.e. fuels like gasoline/petrol and diesel) going up can stand scrutiny.

This “closing of the gap” between the volume of products actually traded in Ghana and the volume of products on which tax is paid is due to SML’s technology and auditing stamping out under-declaration by the fuel marketing companies.

The payment to SML of a percentage of taxes on each unit of these gap-closed volumes makes sense.

In just a few short paragraphs I intend to show that the answer to all three questions is negative. I will further argue that the apparent confusion of eminent professorial specialists in Ghana about these matters is simply due to their neglect of the full range of evidence, especially those outside their specific academic domains.

The logical foundations of the “closing the gap” thesis

In SML’s view, the world before they entered the fuel monitoring picture in 2020 was one in which fuel wholesale and marketing companies routinely hid the true extent of their trading, misrepresented the actual volumes to their primary regulator, the NPA, collected taxes on behalf of the government from traders at the depots and from consumers at the filling stations and, yet, remitted only a small fraction corresponding to only the partial volumes they declared to the regulators and the tax authorities.

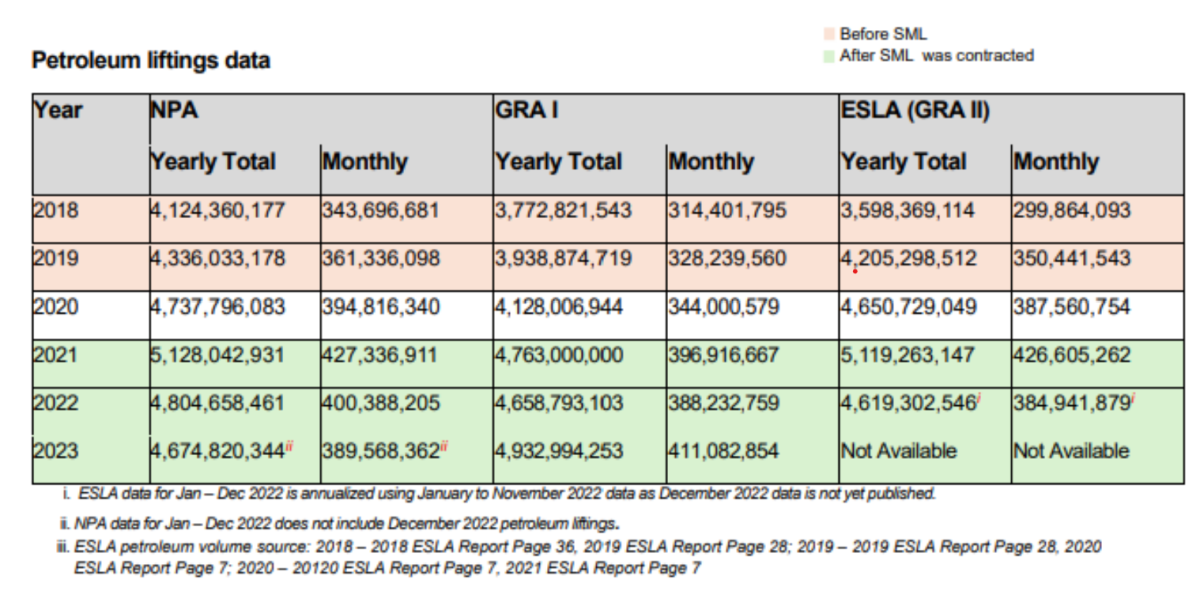

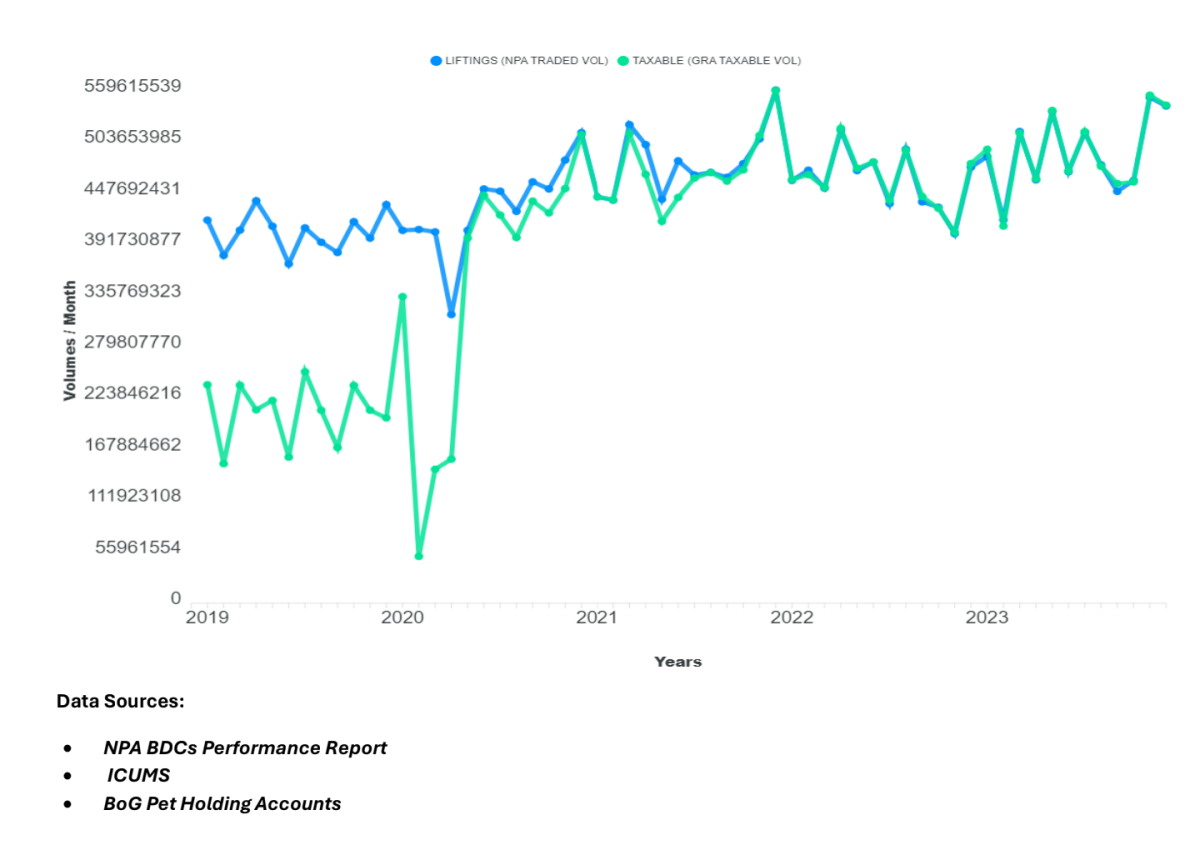

However, look carefully at the charts above. SML and the Finance Dean merely list volumes of fuel declared in the National Petroleum Authority – the main downstream fuel regulator – system (now known by its mouthful name as the Enterprise Relational Database Management System – ERDMS), compare it to the volumes of petroleum for which tax was paid during the financial year as disclosed by the Ghana Revenue Authority (GRA), Ghana’s tax supremo.

It is clear that there is no dispute, per se, of the National Petroleum Authority’s (NPA’s) numbers. In fact, for both the Dean and SML, they provide the benchmark against which the taxable volumes recorded by the Ghana Revenue Authority (GRA) are measured. The problem, then, cannot be that fuel marketing companies are underdeclaring their volumes to the NPA (especially since 2019, the timeframe of their analysis). The real insight is rather that, sometimes, they refuse to remit the tax, due to lax enforcement and compliance.

What then accounts for the apparent improvement in compliance in remitting the taxes collected from consumers (i.e. petroleum levies) and paying the right amount of wholesale tax when loading fuel at the depots (i.e. special petroleum tax) as evidenced by SML’s chart below?

The answer is simple: the growing maturity of the ERDMS model.

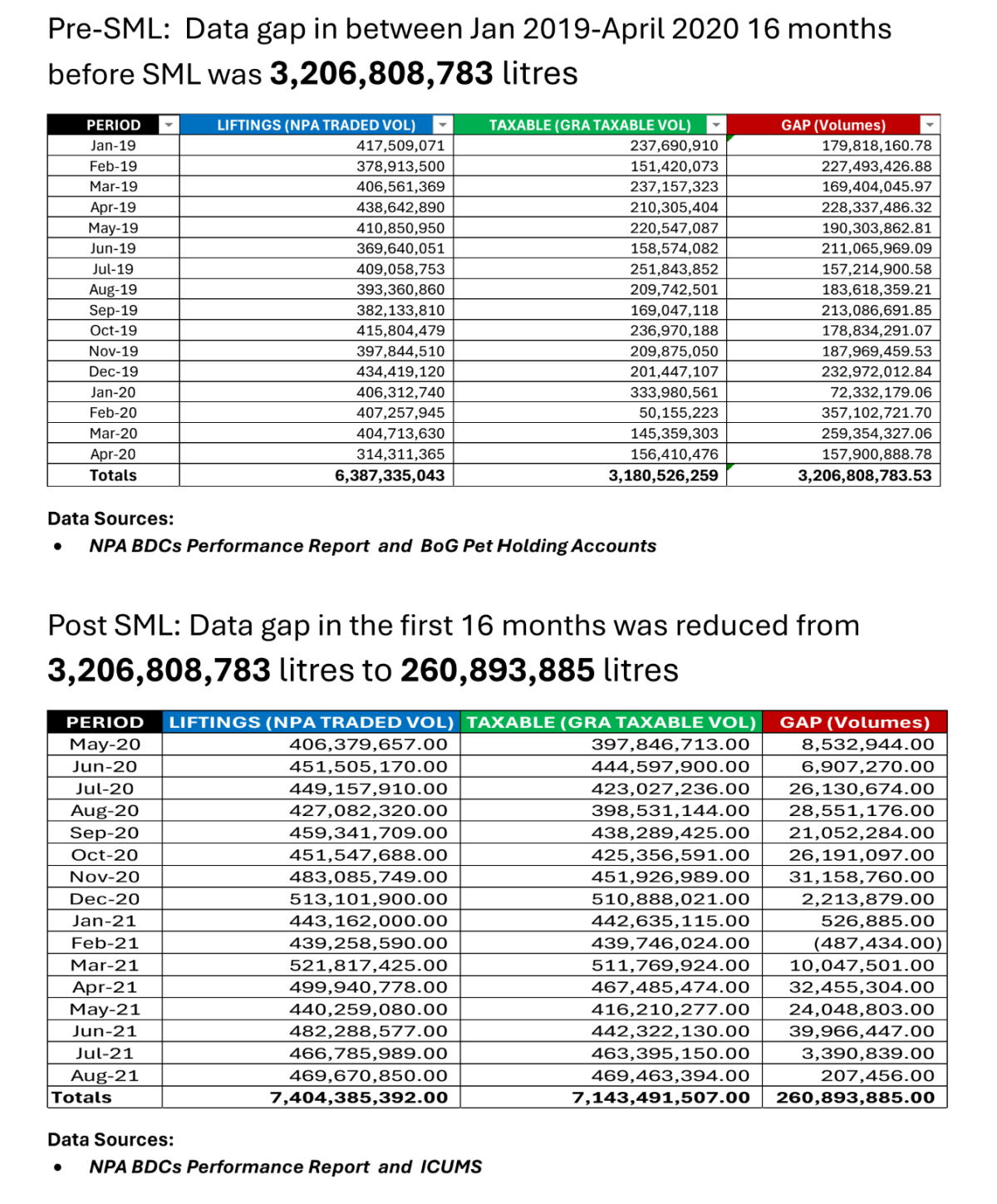

A Change of policy closed the gap

ERDMS is not perfect. However, over the years, it has improved as the NPA gets a firmer handle on it. When it was first launched, following a public tender, it was yet to be proven. The NPA therefore invested public money to improve the system soon thereafter.

A professor of political science or finance, no matter how eminent, who has not followed the NPA and other public sector agencies, or the workings of relevant parliamentary committees, in the petroleum/energy sector closely may not be aware.

Once the ERDMS system became more reliable, the NPA changed policy. It now required that no fuel can be loaded at depots in Ghana and offloaded at retail points without requisite entries into the ERDMS. Some discretion hitherto available to some NPA officers was also curtailed. A “No Tax, No Load” policy began to take shape. Because the ERDMS was being rolled out across all depots, trying to circumvent controls whilst pilling up tax arrears became harder. Over time, as the enforcement measures took hold, the fuel loaded and measured by NPA, and declared in the ERDMS, organically started to converge with the GRA data of petroleum volumes on which tax has been paid.

Beyond Data Entry

Another major challenge that previously led to gaps between what the NPA records as having been lifted and what the GRA can account for taxes on is the problem of losses. Between loading and offloading, various natural technical losses are possible. The NPA recognises evaporation, spillage, leaking, pilferage (or plain stealing by workers at any level), and calibration issues as some of the reasons for routine discrepancies, and even makes provision for “allowable losses”. In some cases, even fuel quality can lead to fuel loaded not being sold, and therefore taxed. As also can temperature changes, which can fool some tank gauges and create discrepancies in volume measurements when none, in fact, exist.

Transhipment, whereby fuel brought into Ghana is sometimes re-exported all create a difference between fuel supplied into the system and fuel actually consumed locally and taxed accordingly. And, of course, not all products carry taxes on them in the first place. Premix is exempted from all taxes, kerosine from most taxes, and MGO from some taxes. Less significant, but real nonetheless, is the fact that fuel used for national security and other public sector purposes can sometimes be hard to fully account for.

If the eminent professors had carefully studied NPA manuals and other process-governing documents across the sector, carefully reviewed submissions to the public corporations’ super-regulator, SIGA, and others, all of these additional causes of variation between the NPA and GRA data would have been obvious. As also is the fact that any of these sources of variations could be heavily impacted by simple policy changes without any shifts in regulatory technology or process.

SML’s magic flowmeters

When pressed to describe what exactly it does and how what it does contributes to preventing losses, under-declarations, or tax evasion, SML spokespersons tend to obfuscate. Not surprising, considering that no fuel trader in Ghana has ever been successfully convicted of under-declaration or fraud using SML data.

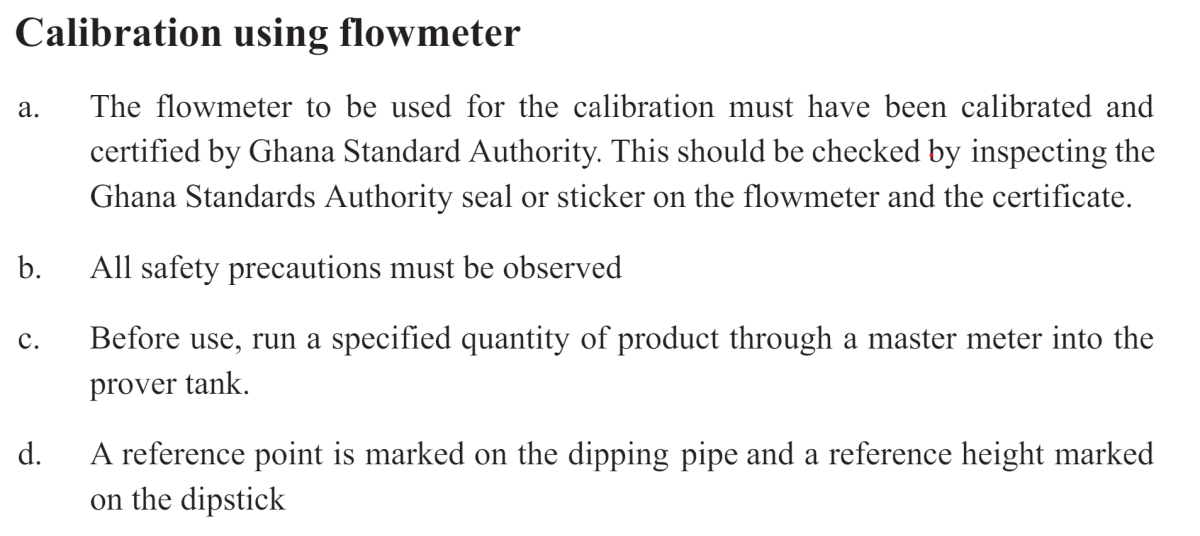

The only thing the media and their interlocutors in civil society have been able to glean so far from such spokespersons is that SML has imported some never-before-seen flowmeters, and associated expertise, from Texas (industry insiders say that these are standard Honeywell equipment), and that these flowmeters are the secret sauce.

Yet, flowmeters abound in the industry, so much so that the NPA requires their use at specific levels of the process chain. Most depots have acquired these and many have subjected them to the required Ghana Standards Authority (GSA) calibration procedure, as dictated by the NPA regulatory guidelines (excerpt below).

What is important is that the NPA should be able to read flowmeters and, where necessary, interface them to its command center so data points from across the supply chain can be integrated for insights.

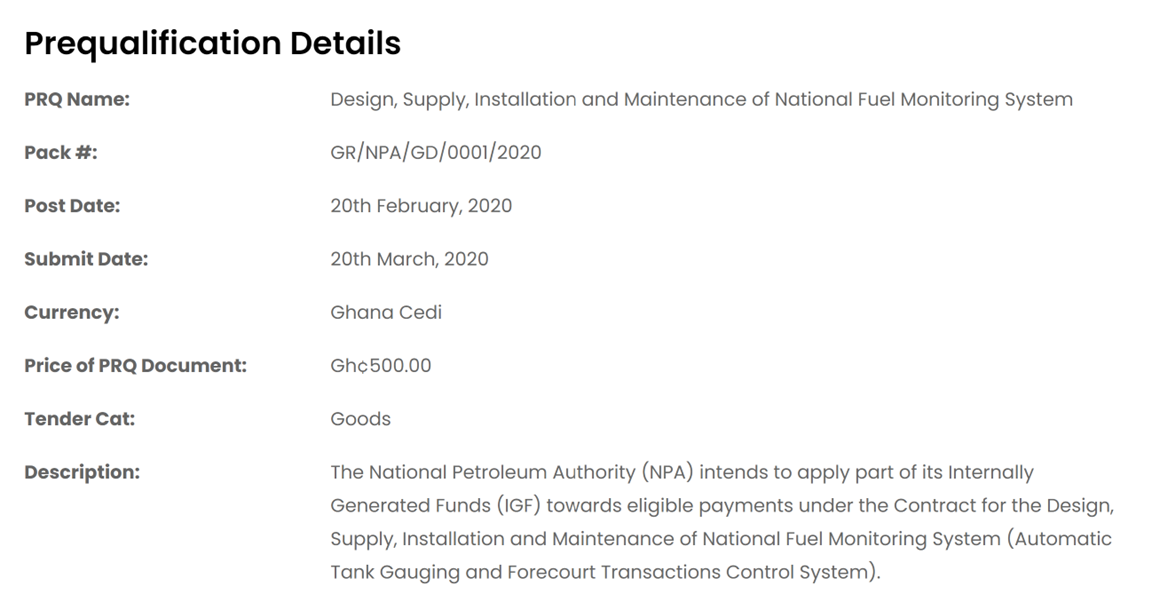

Consequently, in the same year that SML commenced work, NPA began efforts to engage contractors to introduce automated gauges across the supply chain and enhance availability of real-time monitoring data (see sample tender notice below).

Given that, in the end, it is the order information in the ERDMS, connected to the ports platform (ICUMS), which screens the fuel import volumes and classifications in the first place, that is being used to benchmark the GRA’s taxable volumes calculations, it is completely mindboggling that SML and its supporters would insist that existing flowmeters, and those being supplied by the NPA through Rock Africa, even when calibrated by the GSA, cannot supply validation data for the invoice/order data entered into ERDMS by fuel marketing companies as they load, transport, and offload fuel across the country.

Millions of dollars have been spent on schemes of this nature in a bid to more effectively fight fraud, evasion, and circumvention. The strategy of using technology automation for this cause was announced as far back as 2019, and subsequent contracts to the likes of Rock Africa (and its affiliates like Asis) confirm the clear intent of the lead regulator, the NPA, to automate data collection across the fuel distribution network.

End to End system

Like everything else in Ghana, the end to end fuel-monitoring regime is not perfect, but it exists.

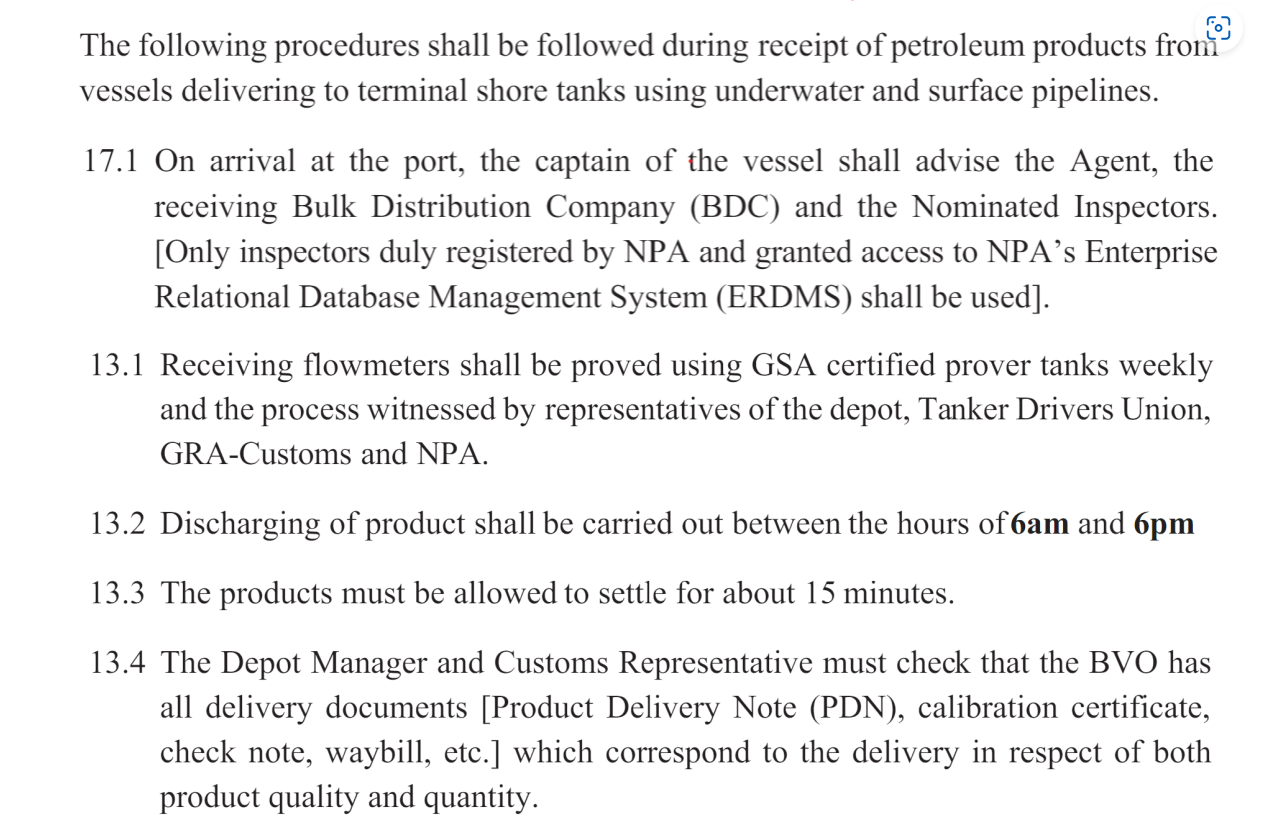

As attested to by the extract below from the NPA’s regulatory guidelines, from the moment a consignment of fuel touches down, the NPA ERDMS – GRA ICUMS integration is activated and information shared between the two systems. As orders are placed and accepted, documents are generated to allow transport of fuel between different points. In fact, the Police and Customs officials have been empowered to stop fuel trucks and demand such documents.

Fuel trucks transiting Ghana must carry special tracking devices connected to NPA’s command centers. Information is regularly exchanged with the security services.

Yes, there are gaps. Like everything else in Ghana. But closing these (real) gaps require that the existing system be improved and that contractors fit into a solution landscape map and add value to the chain. Setting up a totally parallel system for GRA is totally ridiculous when the ideal of sound governance today is “more integrated” government. SML argues that existing systems need to be overseen by it to ensure integrity. But this argument risks descending the whole process into farce. What stops a future administration at GRA or elsewhere in government from demanding another layer of oversight above SML? And issuing yet another “revenue assurance” contract to another company?

Why the taxable volumes increase argument is mathematically deficient

Having addressed the logical issues, we can turn to the statistical analysis, guided by a broad familiarity with the system as a whole and longstanding insights into the operations of government.

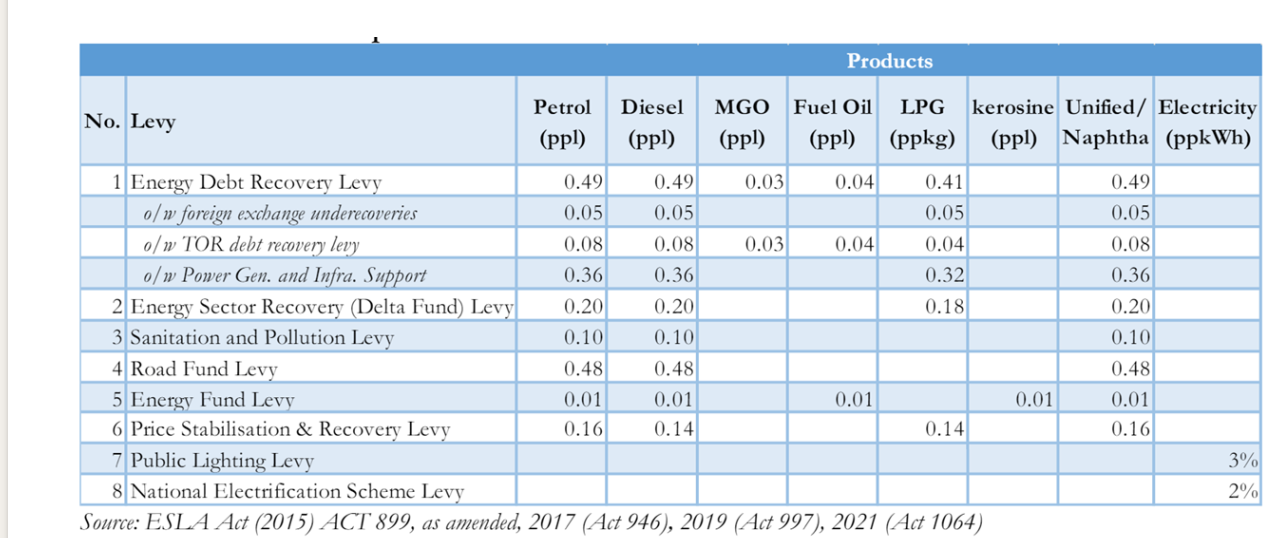

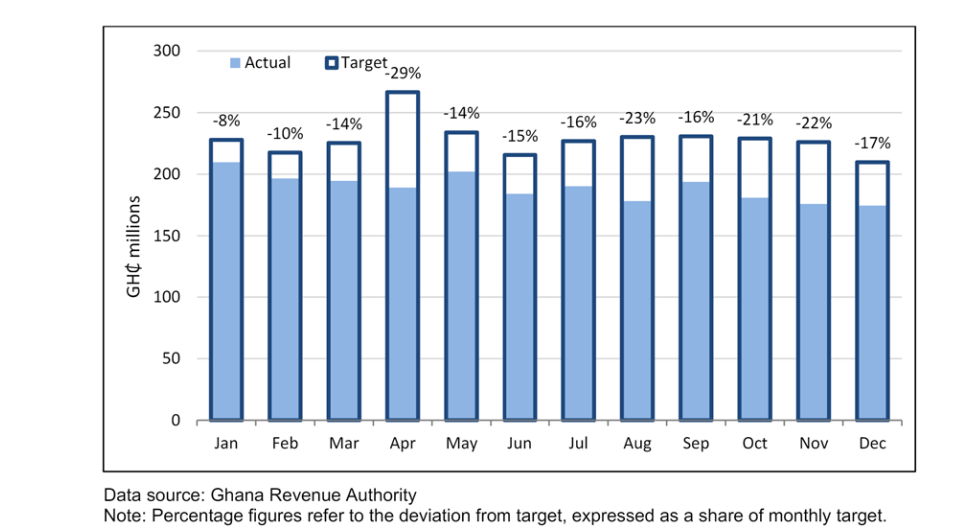

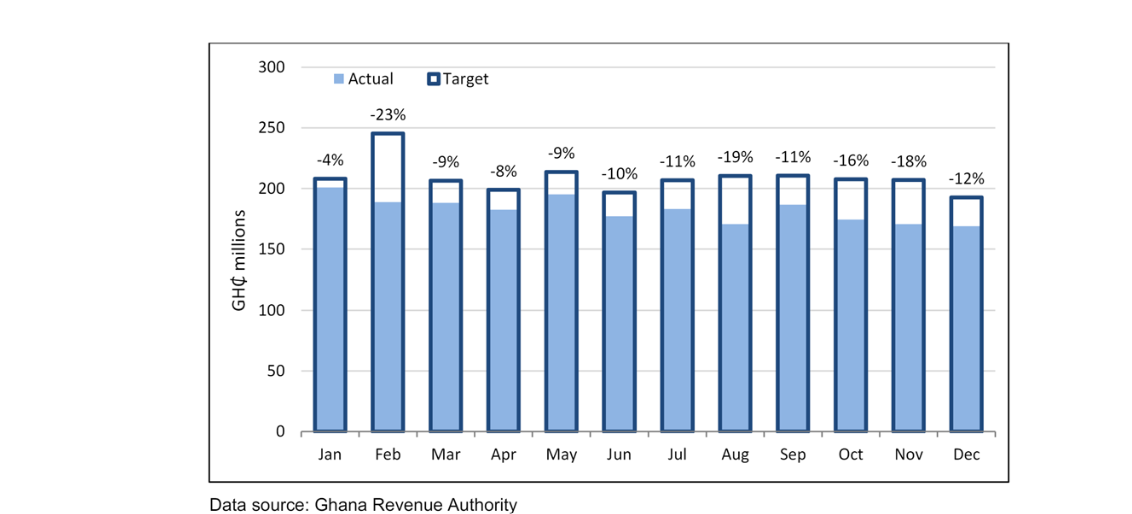

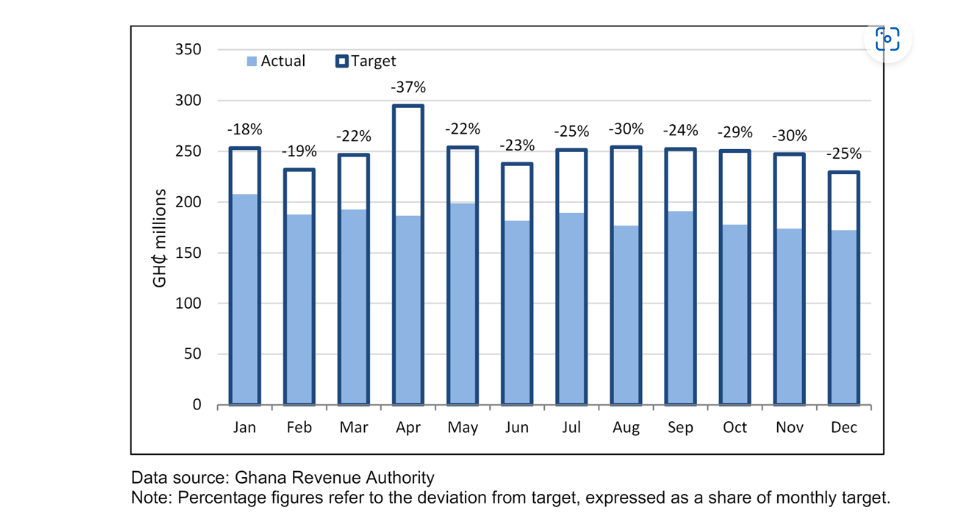

The chart below lists the main taxes on the downstream petroleum sector with the exception of the special petroleum tax charged at the wholesale depot level.

The taxable volumes data being bandied about by SML and assorted SML-supporting professors is usually not disaggregated rendering fuel-specific trends impossible to discern.

SML sometimes creates the impression that they don’t really understand the policy landscape. For example, their spokespersons regularly refer to “petroleum revenue holding funds”, but that term applies only to the upstream sector, and not the downstream sector where they currently operate.

In their writings and media appearances, they fail to separate secular trends from singularities, shocks, and variable patterns. Let us illustrate.

Policy impact on trends

Take two major taxes, the Energy Debt Recovery Levy (ERDL) and Price Stabilisation and Recovery Levy (PSRL). In page 6 of the 2022 ESLA Report (a periodic accounting of petroleum taxes securitised on the bond markets), we learn that:

In 2019, the Energy Debt Recovery Levy (EDRL), Road Fund, and Price Stabilisation and Recovery Levy (PSRL) were revised upwards to correct for the loss in value due to currency depreciation and inflation over the years without a commensurate increase in the fixed specific-type levies in the Price Build-up.

On page 17, we are told that:

i. Low consumption of petroleum products due to high fuel prices at the pumps on account of the surge in prices on the world market (due to the Russia-Ukraine war); and

ii. The removal of the PSRL from the Price Build-Up (PBU) for January 2022 in line with the directive from Government. The PSRL was removed as a means of insulating consumers from paying high cost of fuel at the pump. However, the PSRL was reinstated in February 2022.

Why are both statements critical? Because they illustrate in vivid technicolour how simple policy shifts can dramatically affect petroleum tax revenues irrespective of developments on the regulatory monitoring side, and without regard to SML’s magic flowmeters.

On account of these various factors, with no connection to underdeclaration or tax evasion, petroleum taxes fell considerably between 2021 and 2022, when SML was at post capturing its divine data and powering through its 6-level reconciliation mechanism (according to KPMG).

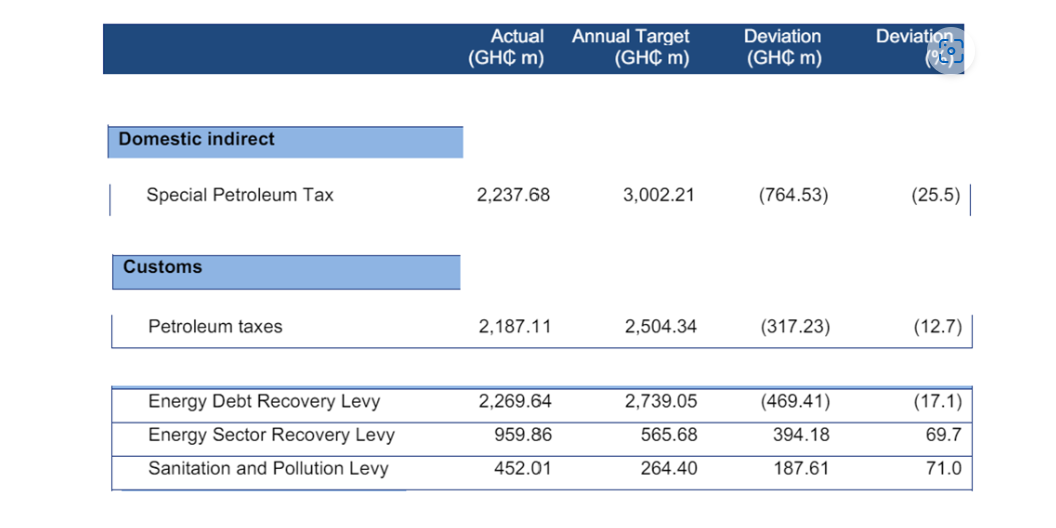

In real terms, according to the GRA’s own data, tax collection for EDRL fell by 26% between 2021 and 2022.

The tax take from the cluster of levies dubbed, “petroleum taxes” dropped by more than 25%.

The depot-level taxes saw an identical level of decline.

Taking SML’s “performance based model”, in which it takes credit for increases and peg its fees to the level of increases, at face value would mean that in 2022 it should have paid a hefty rebate to Government for falling petroleum tax revenue. But, of course, it didn’t.

What is even more intriguing, establishing the policy-primacy of the situation, not all downstream petroleum-related taxes saw a deviation from target (whether or not they fell year to year). Those less affected by certain exogenous factors actually saw an increase in outturn. The sanitation and pollution levy for instance saw a 71% positive uptick against expectations. A professor of finance running some numbers in Stata will miss this if he or she does not have a feel for the ethnographic lay of the land in Ghana’s revenue policy.

Conclusion

In short, it is about time Ghanaians came to understand and appreciate policy analysis as an interdisciplinary domain with its own unique set of contributions to make, independent of the subject matter backgrounds of those who take up the mantle to become policy analysts.

Such individuals and organisations contribute a distinct flavour to the production, processing, and consumption of knowledge in Ghana. Academic specialists of course also have their place. But on certain issues, the brand of policy analysis described in this essay delivers the most poignant insights into what is happening, and, dare I say, what must be done.